Reports & Publications > Financials

Financial Highlights

Sustaining Growth Amid a Challenging Operating Environment

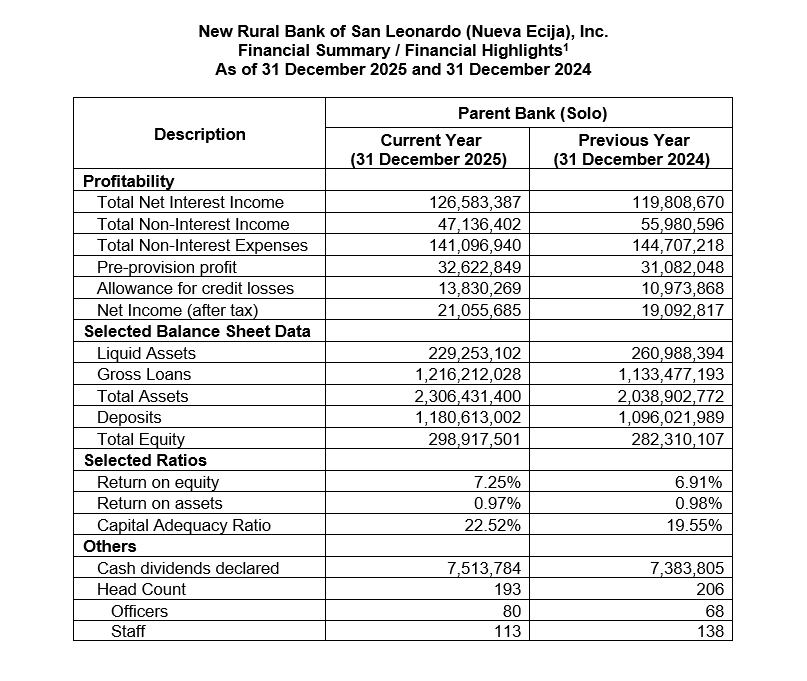

New Rural Bank of San Leonardo (Nueva Ecija), Inc. (NRBSL) delivered another year of positive financial performance in 2025, demonstrating resilience and institutional strength amid a challenging operating environment characterized by persistent inflationary pressures, elevated funding costs, volatile fuel prices, and heightened credit risks affecting both the agricultural sector and rural economies.

Despite these headwinds, the Bank successfully sustained its growth trajectory through disciplined balance sheet management, prudent risk-taking, continued expansion of its core

lending business, and strengthened operational efficiency. The year was marked by improvements in profitability, expansion of earning assets, stronger capitalization, and continued growth in the

Bank's deposit and loan portfolios, all of which reinforce NRBSL's ability to fulfill its dual mandate of financial sustainability and developmental impact.

Profitability Performance

NRBSL posted a net income after tax of ₱21.06 million in 2025, representing an increase of ₱1.96 million or 10.28% over the ₱19.09 million recorded in 2024. The improvement is

particularly noteworthy considering the more conservative provisioning policy adopted during the year and the continued economic uncertainties confronting the Bank's primary markets.

The Bank's core earnings remained robust. Total Net Interest Income increased by 5.65%, rising from ₱119.81 million in 2024 to ₱126.58 million in 2025. This growth was

primarily driven by the expansion of the loan portfolio, improved utilization of interest-earning assets, and sustained demand for credit among agricultural producers, microenterprises, and rural households.

The increase demonstrates the Bank's ability to generate recurring income from its principal business activities despite rising funding costs and competitive market conditions.

While core lending revenues strengthened, Total Non-Interest Income declined by 15.80%, from ₱55.98 million to ₱47.14 million. The reduction reflects lower contributions

from ancillary income sources and non-recurring revenue streams compared with the previous year. NRBSL’s commitment to financial inclusion and relationship banking is a major factor behind this scenario as the Bank

extended reasonable relief by waiving late payment penalties in meritorious and compassionate circumstances where such accommodation promotes borrower recovery and strengthens long-term client relationships.

Despite waivers, the decline in penalty collections did not materially affect overall profitability as the Bank's core banking operations continued to generate stable earnings.

One of the notable achievements during the year was the Bank's continued success in managing operating expenses. Total Non-Interest Expenses decreased by 2.49%, from ₱144.71 million

in 2024 to ₱141.10 million in 2025. This reduction reflects management's efforts to optimize costs, improve operational efficiency, and derive productivity gains from organizational restructuring and process

improvements implemented during the year.

As a result, Pre-Provision Profit increased by 4.96%, reaching ₱32.62 million compared to ₱31.08 million in the previous year. The improvement indicates that the Bank's

underlying operating performance remains strong and continues to provide adequate earnings capacity to absorb credit costs and support future growth.

Consistent with its conservative risk management philosophy, NRBSL increased its Allowance for Credit Losses by 26.03%, from ₱10.97 million to ₱13.83 million.

The higher provisioning reflects management's proactive assessment of emerging portfolio risks arising from inflation, higher production costs, fuel price volatility, and other economic pressures

affecting borrowers. Rather than a sign of portfolio weakness, the increase demonstrates the Bank's commitment to maintaining adequate reserves and safeguarding long-term financial stability.

Balance Sheet Expansion and Asset Growth

The Bank recorded significant balance sheet expansion during 2025, reflecting continued growth in business activities and market penetration.

Total Assets increased by ₱267.53 million, or 13.12%, reaching ₱2.31 billion as of December 31, 2025, compared with ₱2.04 billion a year earlier.

The increase was driven primarily by growth in the loan portfolio and sustained expansion in deposit liabilities, underscoring the Bank's ability to attract resources and deploy them productively.

The Gross Loan Portfolio expanded by ₱82.73 million, or 7.30%, rising from ₱1.13 billion to ₱1.22 billion. Loan growth remained anchored

on the Bank's traditional markets, particularly agriculture, microenterprise, housing finance, and rural consumer lending. The continued expansion of the portfolio demonstrates both the relevance

of the Bank's products and the sustained financing requirements of rural communities despite prevailing economic challenges.

On the funding side, Total Deposits increased by ₱84.59 million, or 7.72%, reaching ₱1.18 billion in 2025 from ₱1.10 billion in 2024. The increase reflects

strong depositor confidence, an expanding customer base, and the effectiveness of the Bank's deposit mobilization programs. In an environment where competition for deposits intensified due to rising interest

rates, the growth achieved by NRBSL underscores the trust reposed by clients in the institution.

Liquid Assets declined from ₱260.99 million to ₱229.25 million, representing a decrease of 12.16%. This movement was largely strategic in nature, reflecting

management's decision to deploy excess liquidity into higher-yielding earning assets, particularly loans. The reduction should therefore be viewed within the context of active balance sheet management

rather than liquidity weakness, as the Bank continued to maintain adequate liquidity levels throughout the year.

Capital Strength and Shareholder Value

NRBSL further strengthened its capital position in 2025, reinforcing its capacity to absorb risks, support future expansion, and comply with increasingly stringent regulatory standards.

Total Equity increased by ₱16.61 million, or 5.88%, from ₱282.31 million in 2024 to ₱298.92 million in 2025. The growth was primarily driven by retained earnings

and continued profitability, reflecting the Bank's ability to generate capital internally while maintaining shareholder returns.

A particularly significant achievement during the year was the improvement in the Bank's Capital Adequacy Ratio (CAR), which increased from 19.55% to 22.52%. This level

is substantially above regulatory minimum requirements and provides a strong capital buffer against potential economic shocks and credit risks. The higher CAR likewise enhances the Bank's capacity to

support future asset growth and pursue strategic opportunities.

Return on Equity (ROE) improved from 6.91% in 2024 to 7.25% in 2025, indicating more effective utilization of shareholders' capital and stronger value creation. Although

Return on Assets (ROA) remained relatively stable at 0.97%, compared with 0.98% in the previous year, the ratio reflects the Bank's continued ability to generate earnings while supporting

significant balance sheet expansion.

The Bank also maintained its commitment to rewarding shareholders through regular dividend distributions. Cash dividends declared amounted to ₱7.51 million in 2025, slightly higher

than the ₱7.38 million declared in 2024, reflecting confidence in the Bank's earnings capacity and financial position.

Organizational Strengthening and Human Capital Development

During 2025, NRBSL continued its organizational optimization and capability-building initiatives aimed at improving efficiency, accountability, and succession readiness.

Total manpower declined from 206 employees in 2024 to 193 employees in 2025. However, the composition of the workforce underwent a significant shift. The number

of officers increased from 68 to 80, while staff positions decreased from 138 to 113. This change reflects management's deliberate effort to strengthen supervisory and managerial

capacity, improve leadership depth, and align organizational resources with the Bank's strategic priorities.

The organizational restructuring initiative is expected to support stronger governance, improved execution discipline, enhanced risk management oversight, and more

efficient service delivery across the organization.

Overall Assesment

The Bank's 2025 performance reflects a year of disciplined growth, prudent risk management, and institutional strengthening. Despite economic uncertainties, higher provisioning

requirements, and softer non-interest income generation, NRBSL successfully improved profitability, expanded its balance sheet, strengthened capitalization, and enhanced operating efficiency.

The growth in loans, deposits, assets, and equity demonstrates the continued confidence of clients, regulators, partners, and shareholders in the Bank's business model and strategic

direction. Equally important, the Bank maintained strong capital buffers and adopted conservative provisioning practices, ensuring that growth remains sustainable and risk-conscious.

Taken together, these results underscore NRBSL's resilience as a development-oriented financial institution and reinforce its capacity to continue advancing its mission of promoting

financial inclusion, supporting agricultural modernization, empowering rural enterprises, and contributing to countryside economic development. As the Bank enters the next phase of its growth journey,

it remains well-positioned to navigate emerging challenges while creating long-term value for its stakeholders and the communities it serves.